Have you ever looked at your bank account and felt a pang of frustration? You’re working hard, putting money aside, but it seems to be growing at a snail’s pace. Meanwhile, you hear stories of people who seem to be effortlessly building wealth. The difference often lies in a single, critical decision: whether to simply save your money or to put it to work. The question of Investing vs. Saving: Which One Helps You Grow Faster? is at the heart of every financial journey.

This article is your definitive guide to understanding the fundamental difference between these two strategies. While both are crucial components of a healthy financial life, they serve different purposes and offer dramatically different outcomes. We’ll break down what each strategy entails, compare their pros and cons, and help you determine which approach is right for your specific goals. By the end, you’ll have a clear roadmap to not just accumulate money, but to actively build wealth that can secure your future and turn your financial dreams into reality.

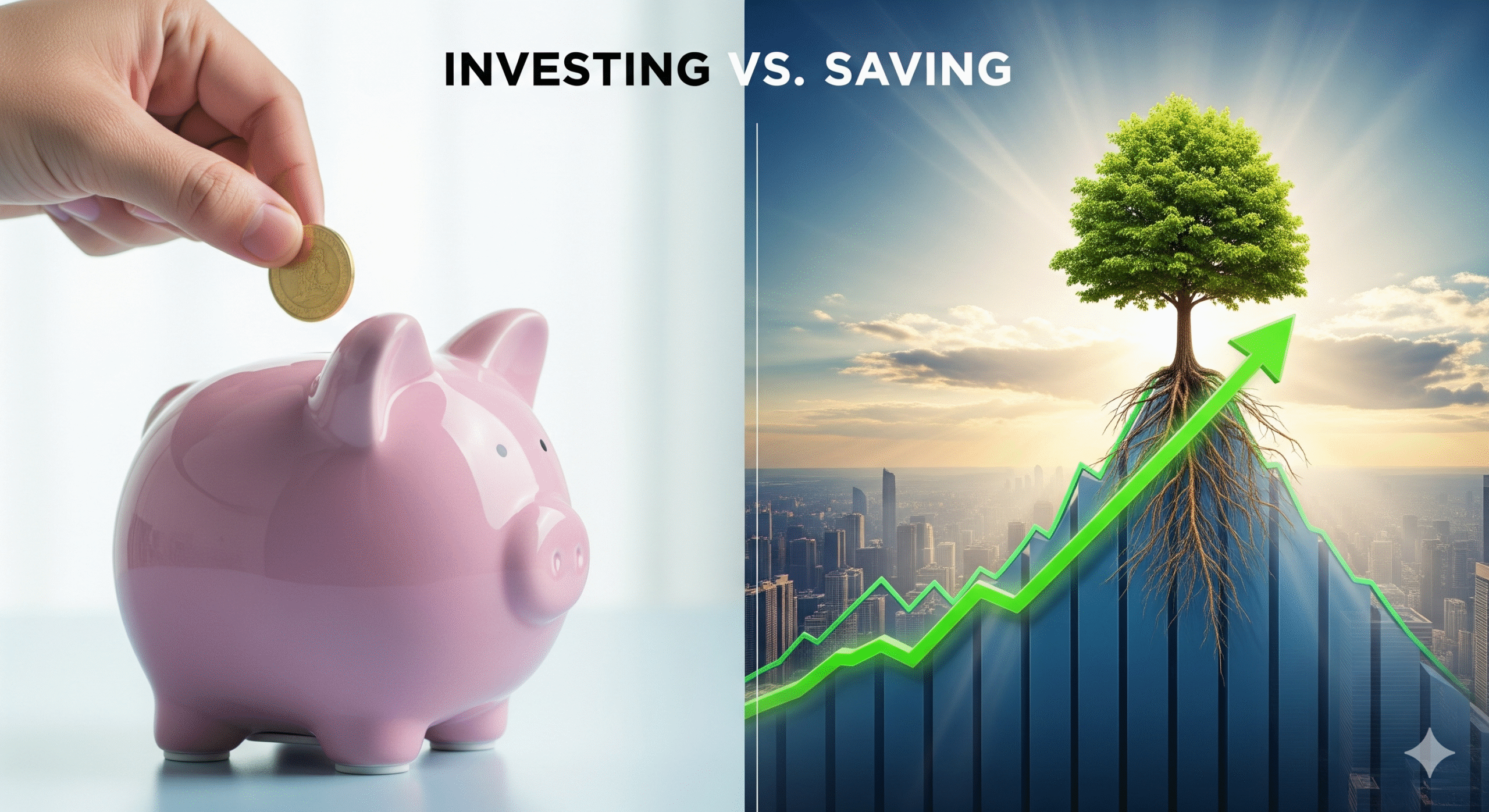

Background and Context: The Silent Enemy of Your Money

Before we dive into the comparison, we must first understand why the old-school approach of “just saving” is no longer a viable long-term strategy for building wealth. The silent enemy is inflation. Inflation is the gradual increase in prices for goods and services over time, which means that the purchasing power of a dollar decreases. A dollar you saved in 2020 buys less today than it did then.

A traditional savings account, while safe and secure, offers a return that is typically far below the rate of inflation. This means that even though the number in your account might be getting bigger, your money is actually losing value in real terms. You’re losing the purchasing power you’ll need for your future self.

This is where the distinction between saving and investing becomes so crucial. Saving is about setting money aside for a specific purpose or an emergency. It’s a foundational step. Investing, on the other hand, is about putting that money to work in a way that generates returns that outpace inflation, allowing your wealth to grow. It is the engine of true financial progress.

Detailed Comparison: A Head-to-Head Breakdown

While the lines can sometimes blur, saving and investing are fundamentally different activities. Let’s compare them across a few key metrics to highlight their unique roles.

| Aspect | Saving | Investing |

| Primary Goal | Safety & Preservation: The main goal is to protect your capital. It’s for short-term needs and emergencies. | Growth & Wealth Creation: The main goal is to make your money grow, often at a rate that beats inflation. |

| Risk Level | Very Low to Zero: Your principal is typically protected by deposit insurance (e.g., FDIC in the U.S.). | Variable: Ranges from low-risk (government bonds) to high-risk (individual stocks, cryptocurrencies). There is always a risk of losing a portion or all of your principal. |

| Return Potential | Low: Returns are minimal, often just enough to keep pace with a small fraction of inflation. | High: Returns can range from a few percent to double digits annually, with a long-term average historically around 8-10% for the stock market. |

| Accessibility & Liquidity | Very High: Funds are almost always immediately available for withdrawal without penalty. | Variable: Some investments are highly liquid (stocks), while others are not (real estate). Cashing out can sometimes trigger a fee or tax event. |

| Time Horizon | Short-Term: Best for goals within the next 1-3 years, such as a down payment on a car or a vacation fund. | Long-Term: Best for goals 5+ years in the future, such as retirement, a child’s education, or buying a home. |

| Effort Required | Low: Simply involves depositing money into a bank account. | Moderate to High: Requires research, continuous monitoring, and strategic decision-making, though this can be simplified with automated tools. |

Export to Sheets

The key takeaway is that saving is for preserving your money, while investing is for growing it. Understanding this distinction is the first and most important step to mastering your personal finances.

Key Features and Benefits: The Rewards of Each Strategy

Both saving and investing offer unique benefits, and a wise financial plan uses them in concert.

The Power of Saving: Your Financial Foundation

Saving is the bedrock upon which all other financial strategies are built. It provides a crucial sense of security and a solid foundation for your financial goals.

- Emergency Fund: An emergency fund is non-negotiable. This is money saved for a rainy day, such as a job loss, a medical emergency, or an unexpected home repair. These funds must be immediately accessible and risk-free.

- Safety and Peace of Mind: Knowing your money is in a secure, insured account provides peace of mind. You don’t have to worry about market fluctuations or losing your principal.

- Funding Short-Term Goals: If you’re saving for a down payment on a car next year or a trip in six months, a high-yield savings account is the perfect place for that money. You can’t risk putting it in the stock market and having it drop right before you need it.

The Power of Investing: The Engine of Growth

If saving is your foundation, investing is the engine that drives you towards financial freedom. Its primary benefit is the power of compounding.

- Compounding Returns: This is often called the “eighth wonder of the world.” Compounding is the process of earning returns on your initial investment and on the returns you’ve already earned. For example, if you invest $1,000 and it grows by 10% in a year, you now have $1,100. In the next year, you’ll earn 10% on the full $1,100, not just the original $1,000. Over decades, this creates an exponential growth curve that is impossible to achieve through saving alone.

- Outpacing Inflation: A well-diversified investment portfolio, particularly in stocks, has historically delivered returns that are well above the rate of inflation. This ensures your money retains and even increases its purchasing power over time.

- Building Generational Wealth: Investing is not just about building a retirement nest egg. It’s about creating enough wealth to leave a legacy for your family and to have the freedom to pursue your passions without financial constraints. It transforms your money from a static number into a dynamic tool for growth.

Pros and Cons: A Look at the Flip Side

Every financial strategy has its trade-offs. It’s important to understand them fully before making a decision.

Saving: The Good and the Bad

- Pros:

- Safety: Your money is insured and protected from market volatility.

- Simplicity: It’s incredibly easy to do. There’s no research or strategic decision-making required.

- Liquidity: You can access your money whenever you need it without any penalties or delays.

- Cons:

- Low Returns: The interest rate is typically so low that it can’t keep up with inflation.

- Loss of Purchasing Power: Over the long term, your money will be able to buy less than it can today.

- Missed Opportunity: You miss out on the incredible growth potential of the market.

Investing: The Good and the Bad

- Pros:

- High Growth Potential: Investing offers the best chance of building significant wealth over the long term.

- Hedge Against Inflation: It’s the most effective way to ensure your money retains its purchasing power.

- Passive Income: Many investments, such as dividend stocks or rental properties, can provide a steady stream of passive income.

- Cons:

- Risk of Loss: The market can be volatile, and you can lose money, especially in the short term.

- Requires Knowledge and Discipline: You need to do your research, stay disciplined during market downturns, and have a clear strategy.

- Fees and Taxes: Investing can come with fees (management fees, trading costs) and taxes on capital gains.

Use Cases: Who Should Be Doing What?

It’s not a question of Investing vs. Saving but rather a question of knowing when to do each. A smart financial plan integrates both strategies at different stages and for different goals.

When to Save: The Foundational Layer

- The Emergency Fund: This is always the first and most important step. You should aim to save 3-6 months of living expenses in a high-yield savings account. This is your safety net.

- Short-Term Goals: If your goal is to buy a car in a year, save for a down payment on a house in 2-3 years, or pay for a vacation next summer, then a savings account is the appropriate place for that money. The low-risk, high-liquidity nature of a savings account is perfect for this purpose.

- High-Interest Debt Repayment: Before you start investing, it’s often wise to pay off high-interest debt, such as credit card debt. The interest rate you pay on that debt is often much higher than the return you could get from investing.

When to Invest: The Growth Engine

- Retirement: This is the ultimate long-term goal. If you are 5, 10, or 20+ years away from retirement, investing in a diversified portfolio of stocks and bonds is the only way to ensure your money will have the purchasing power you’ll need.

- Children’s Education: A college fund is a great long-term goal for investing. You can use tax-advantaged accounts like a 529 plan to invest money for your child’s education years in advance.

- Building a Legacy: Once your emergency fund is full and your short-term goals are on track, the remaining money should be invested. This is how you build true wealth that can be passed down to future generations and provide you with a life of financial freedom.

FAQs: Your Most Common Questions Answered

Q1: Is saving money a waste of time?

A: No, absolutely not. Saving is the essential first step. You need a cash reserve for emergencies and short-term goals. Without that, you would be forced to sell your investments at an inopportune time, which could be a huge financial mistake. Investing vs. Saving isn’t a competition; they are partners.

Q2: What is a good return on investment?

A: A “good” return depends on the type of investment and your risk tolerance. Historically, the S&P 500 (a broad index of the U.S. stock market) has averaged around 8-10% annually over the long term. While you may not get that every year, it’s a good benchmark to aim for.

Q3: How do I start investing with little money?

A: You can start investing with very little money. Many brokerage firms allow you to open an account with no minimum deposit. You can use an app to buy fractional shares of expensive stocks. The most important thing is to start, even if it’s just with $20 a month. Time is your greatest asset due to the power of compounding.

Q4: Should I pay off debt or invest?

A: As a general rule, if your debt has a high-interest rate (e.g., credit card debt), you should focus on paying it off first. The guaranteed return from paying off that high-interest debt is likely greater than the potential return from investing. If your debt has a low-interest rate (e.g., a mortgage), it may be better to invest in the stock market instead.

Q5: What’s the difference between a savings account and a money market account?

A: A money market account (MMA) is similar to a savings account but often offers a slightly higher interest rate and may have some limited check-writing capabilities. However, it may also require a higher minimum balance and could have some restrictions on withdrawals. Both are considered very low-risk.

Q6: Can I lose all my money when I invest?

A: It is possible to lose money, yes. However, a well-diversified investment portfolio—one that includes a variety of stocks, bonds, and other assets—significantly reduces this risk. The key is to never put all your eggs in one basket.

Conclusion: A Balanced Approach to Financial Growth

The question of Investing vs. Saving isn’t an either-or proposition. It’s about understanding the unique role of each strategy in your financial life. Saving is for the short term, providing a safety net and liquidity for your immediate needs. Investing is for the long term, serving as a powerful engine for wealth creation that can outpace inflation and turn your future dreams into reality.

A successful financial plan uses a balanced approach. First, you save to build your emergency fund. Second, you pay off high-interest debt. Third, you begin to invest consistently for your long-term goals. This three-step process is the most effective way to protect your money while ensuring it works as hard for you as you work for it.

Final Verdict: Investing is the Key to True Wealth

The final verdict is clear: if your goal is to simply have money, you should save. But if your goal is to build wealth and secure your financial future, you must invest. Saving provides security, but investing provides freedom. By understanding and implementing the principles of both, you are taking control of your financial destiny, ensuring that you’re not just holding on to money, but actively and strategically growing it for the life you want to live.